01

Language Barriers

Mid level developers face language barriers and low comfort with digital tools

HDFC Bank · Lead Product Designer

Translating a legacy manual workflow into a streamlined, fully digital experience. By tackling market-specific challenges and balancing business needs for accelerated approvals and improved transparency.

Overview

HDFC's disbursement toolchain was fragmented across agents, spreadsheets, and legacy screens—a poor fit for high-volume tower projects—so borrowers and builders lacked a single coherent path from initiation to disbursement.

What I did?

Stakeholder map: product, operations, marketing, and customer success connect above the lead product designer; sales, legal, engineering, and finance connect below — one hub in the middle.

0

months0

Users onboarded inside the first operational yearLead Product Designer

Over 80% of India's urban housing market is driven by large multistory apartment projects — hundreds of units per property, multiple developers, thousands of customers, all moving through the same loan pipeline.

HDFC's existing system wasn't built for this. It was built for single-unit listings, and it showed. Loan applications moved through a patchwork of agents, spreadsheets, and legacy screens

Build a fully digital workflow that eliminates agent dependency, reduces processing time, and scales with growing loan volume. Provides loan visibility, transparency, and trust for users and business owners.

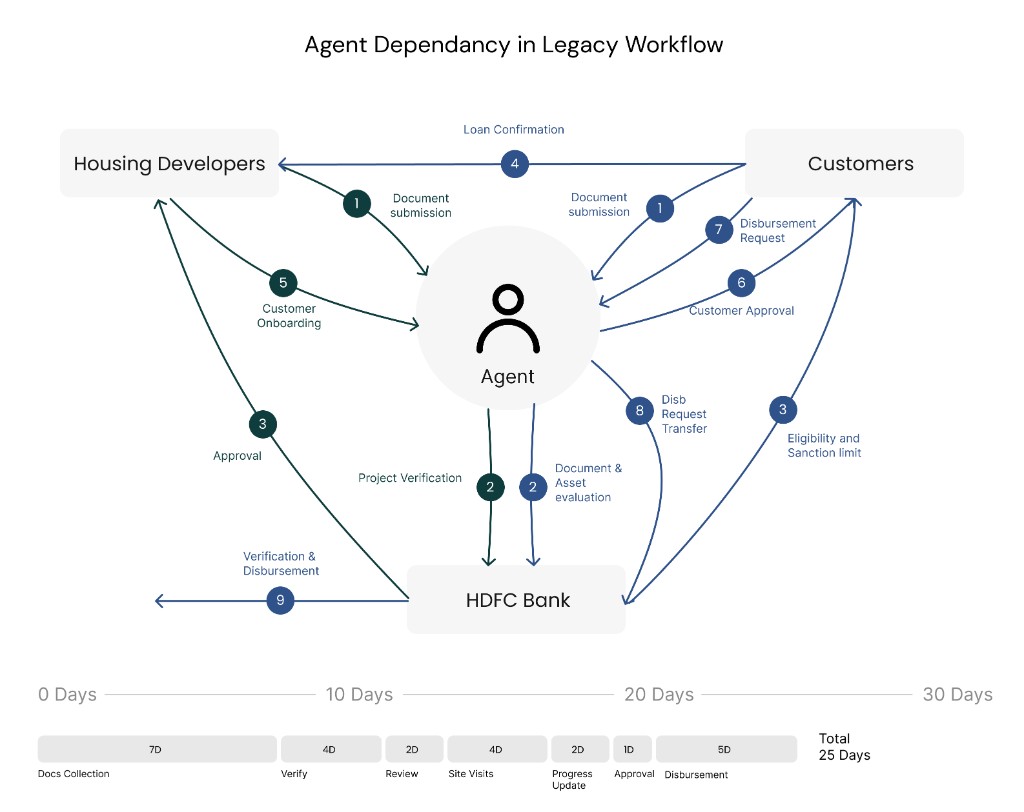

Here's what a housing developer's loan journey looked like before this platform existed:

A developer submits documents through an agent. The agent forwards them to the bank. Somewhere inside, the application enters a queue no one outside can see. Days pass. The developer calls the agent. The agent calls the bank. Nobody has a clear answer. More days pass. A document is missing — but no one told the developer, so they're still waiting. By the time the correction is made, weeks have gone by.

Problem

Solution

We interviewed housing developers across six cities — Mumbai, Delhi, Bangalore, Chennai, Hyderabad, and Pune — ranging from boutique developers with two ongoing projects to firms managing hundreds of units simultaneously.

Three things came up in every single conversation:

Mid level developers face language barriers and low comfort with digital tools

This dependency suggests the existing ecosystem doesn't meet user needs

Users experience frustration due to absence of direct visibility into loan status

India's urban housing market is dominated by large multistory apartment projects (over 80%) involving hundreds of units per property.

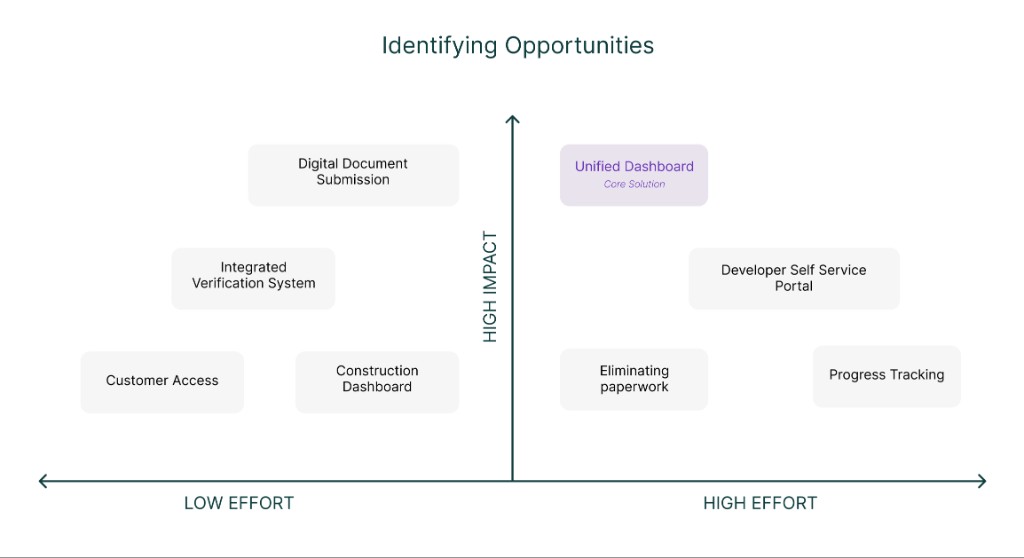

Placeholder: brief narrative on the main gaps between user needs and the current experience, and how those informed the opportunity areas explored in the matrix.

| Business Needs | Balancing Both | User Needs |

|---|---|---|

1. Data Entry Across Departments Each department (Credit, Legal, Technical, Disbursement) wanted their own data fields and forms to ensure complete information capture and accountability. | Designed a solution where shared fields auto-populate across departments. Introduced role-based views — each department could add specific fields without duplicating user input. This maintained departmental control while creating a seamless user flow. | Customers and relationship managers wanted to avoid filling or uploading the same information repeatedly during the loan journey. |

2. Disbursement Compliance The business wanted strict audit trails and manual checkpoints before releasing funds to developers to ensure compliance with RBI and internal audit norms. | Implemented a semi-automated disbursement request flow — developers could trigger a request by uploading progress proofs, and the system would auto-validate completeness before sending for manual approval. This reduced delays while retaining compliance checkpoints. | Developers wanted faster disbursement processing once milestones were achieved, avoiding manual back-and-forth. |

3. Loan Status Transparency Departments wanted control over when status updates were visible externally to avoid premature disclosure of internal decisions. | Created a tiered visibility model — certain statuses (like “under review” or “awaiting approval”) were automatically shared with customers, while sensitive backend updates remained internal until finalized. This built transparency without compromising internal control. | Customers wanted real-time updates to reduce uncertainty and constant follow-ups. |

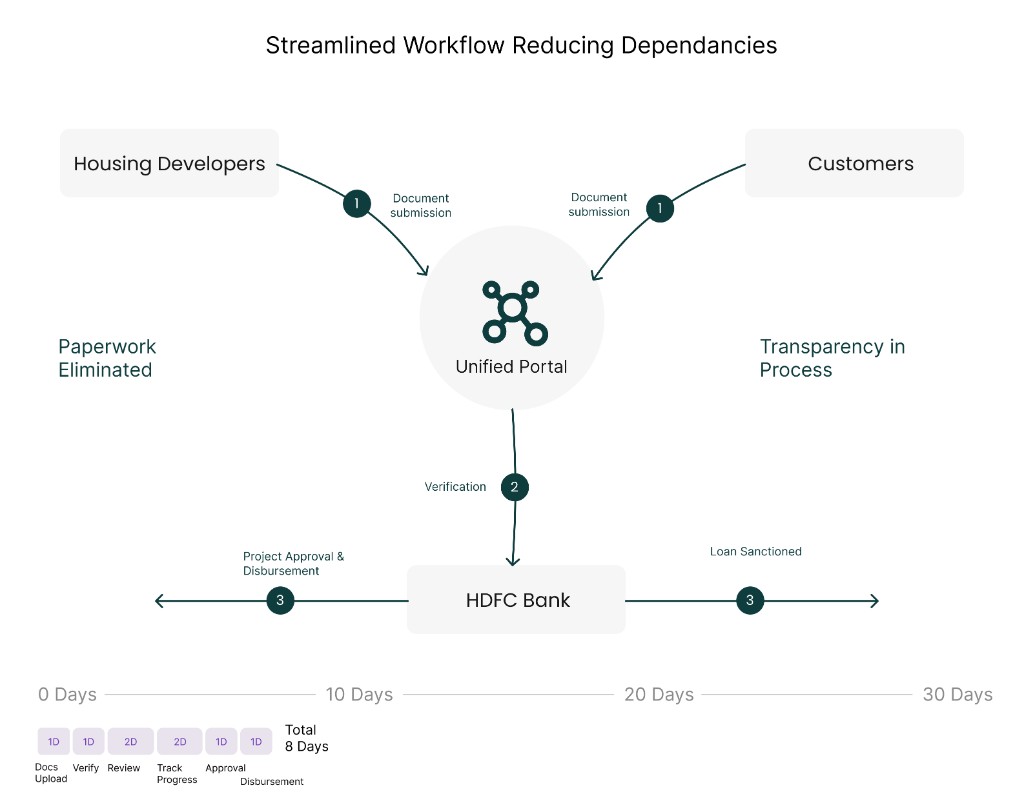

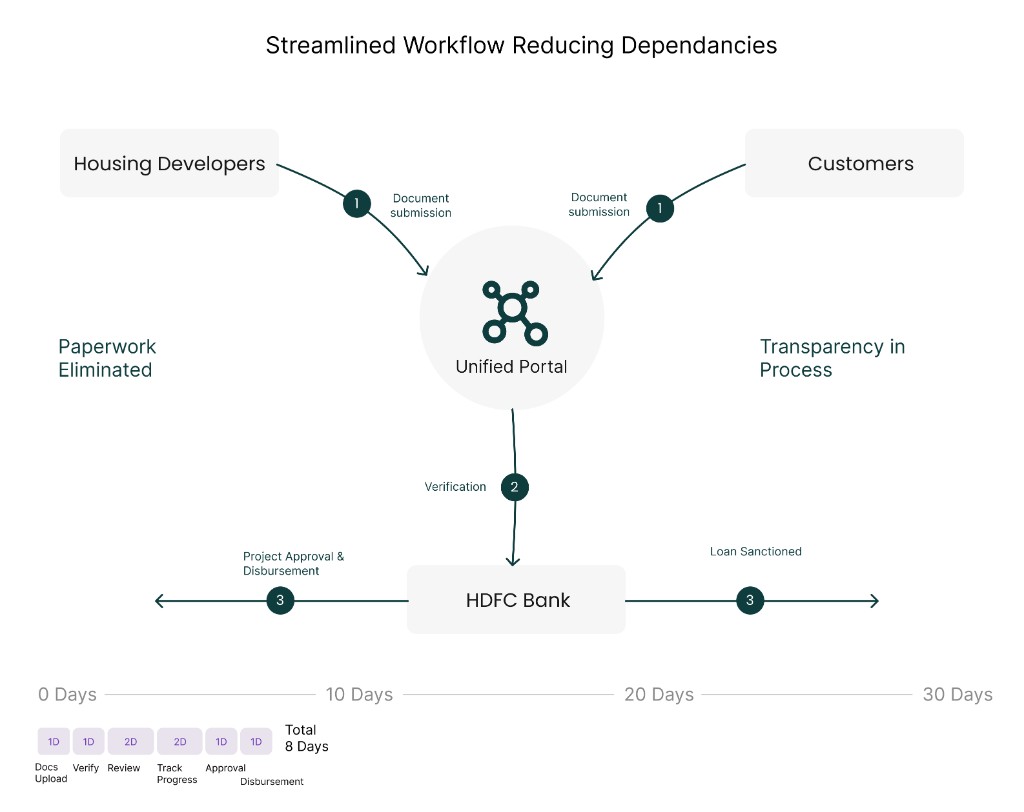

This workflow transforms the fragmented, agent-dependent manual process into a unified digital ecosystem that reduces processing time from 30 days to just 8 days—a 73% improvement—while eliminating dependency on bank agents as intermediaries.

We worked closely with stakeholders in an iterative, back-and-forth process to co-create a clear and intuitive information structure. We aligned on user needs, business goals, and content priorities, ensuring the architecture supported seamless navigation and discoverability across the platform.

Reduced workflow steps through guided paths, dashboards, and inline validation so analysts spend time on judgment, not data wrangling.

Clear status timelines, disclosures, and feedback patterns so borrowers and developers understood where they stood.

Component-based patterns and repeatable templates adapted as new projects and corridors onboarded.

Kept HDFC analysts, borrowers, builders, and field teams united in shared objects and statuses.

Planned offline edge cases and exception flows so disruptions did not deadlock disbursement.

Plain-language copy, multilingual consideration, and legible hierarchies lowered barriers for junior staff and borrowers.

Users can view projects and locate them on a map — surfacing approvals, timelines, and project health at glance.

Users can view tower listing, customer details, and request disbursements.

Developers keep banks informed about construction status with structured milestones.

Harmonizing underwriting logic with humane status communication proved as important as optimizing screen flows — accelerating adoption required making the invisible bureaucracy legible across every stakeholder.